Brent Breaches $82 — and Analysts Fear $120 Is Next

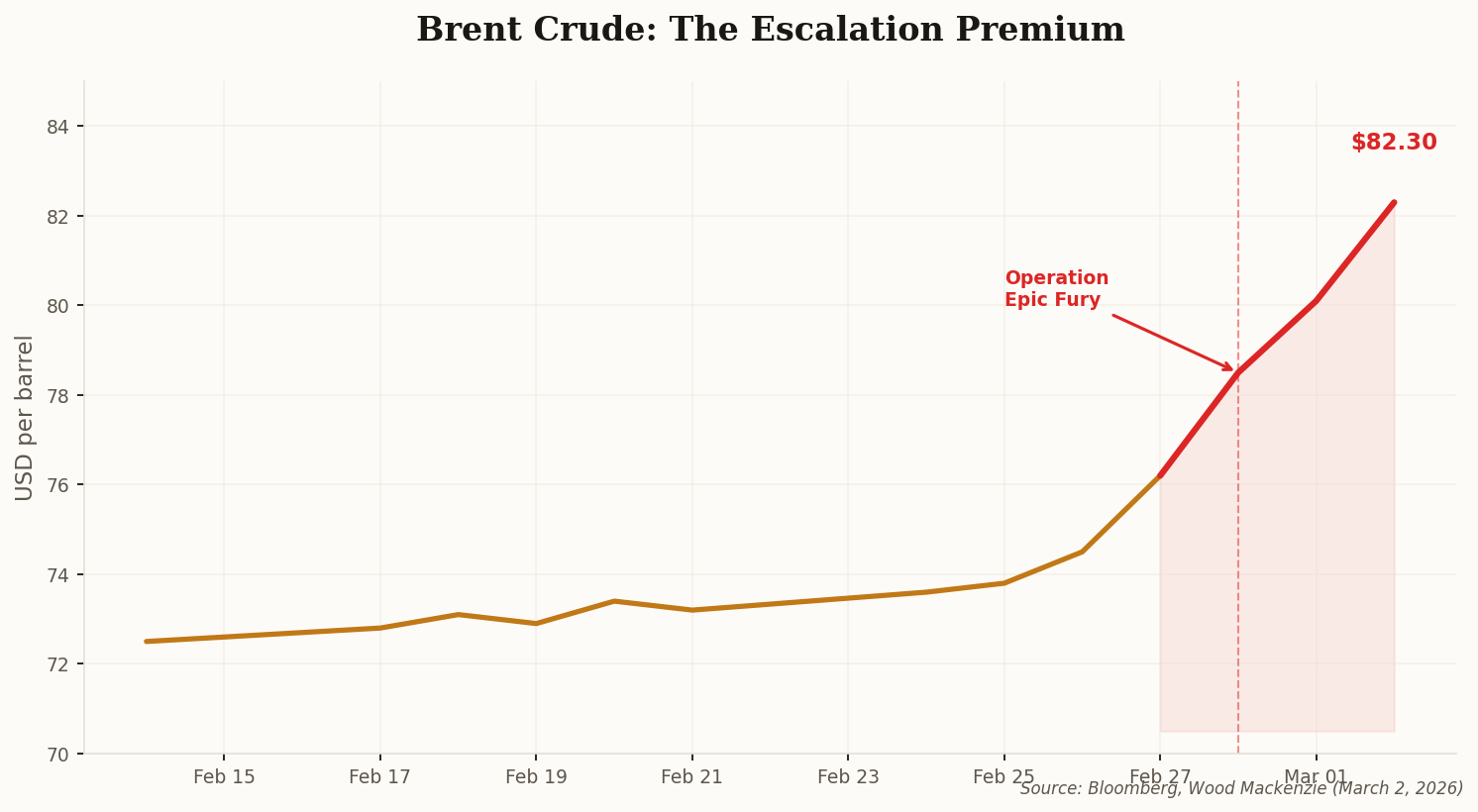

When Operation Epic Fury launched on February 28, oil traders didn't wait for confirmation of supply disruptions. They priced them in immediately. Brent crude surged between 10% and 13% in the first trading sessions of March, briefly topping $82 per barrel — a level that looked unthinkable two weeks ago when oil was languishing in the low $70s.

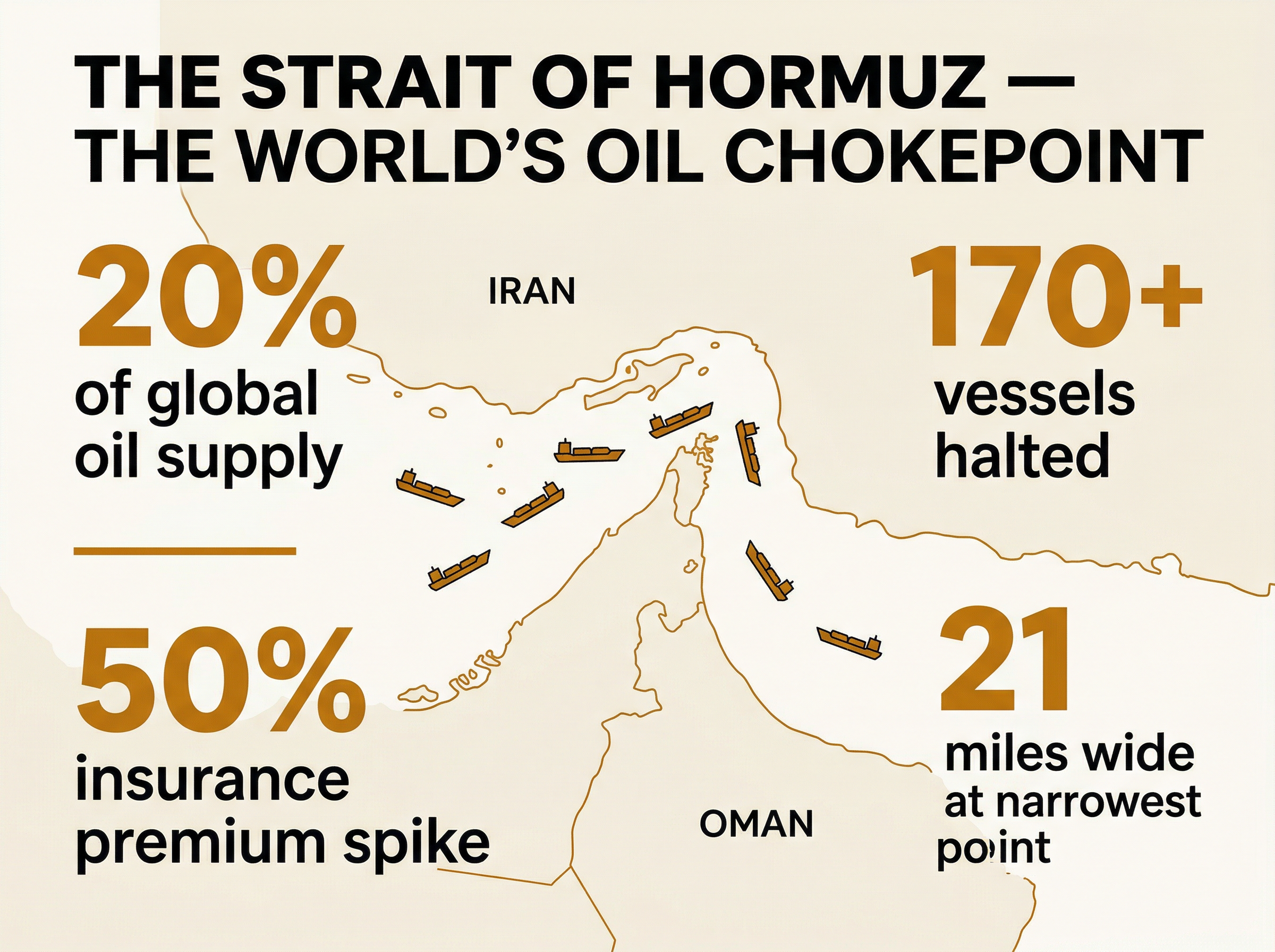

The number that should keep you up at night isn't $82. It's $120. That's where Wood Mackenzie analysts project prices could land if the Strait of Hormuz — through which 20% of the world's oil supply transits daily — faces a prolonged blockade. "The market is pricing in a worst-case scenario where 20% of the world's oil supply is effectively sidelined," one commodity strategist told Bloomberg.

The critical variable is duration. A 48-hour flare-up fades from trading screens within a week. A sustained campaign through Hormuz territory rewrites global energy economics for a generation. Every day the strait remains effectively closed adds roughly $2-3 to the per-barrel price floor, according to energy analysts. This isn't 2020's demand destruction in reverse — it's supply destruction, the kind that doesn't respond to OPEC phone calls or SPR releases.